The balance sheet is one of the most critical documents that any person will learn at any accounting related course or initial finance course. The foundation of financial reporting, but many students struggle to understand at first glance. Grasping knowledge of how to prepare a balance sheet is a stress free task. You can learn this skill easily if you have the proper format, definitions, and an example of its use. This guide teaches the process of creating a balance sheet step-by-step with simple explanations, and then a detailed example of the balance sheet developed specifically for beginners.

What Is a Balance Sheet? The Accounting Equation

A formal financial statement that summarizes the money's situation of a company at a particular moment in time is called a balance sheet. It is like a snapshot - a date to capture the business's assets, liabilities and the remaining interest of the owner(s). When compared to income statement which represents the statement about the activities related to particular period of time, the Balance Sheet is that statement of activities that show work on that one moment or instance of times such as “As of December 31” or “As of March 31.”

It is one of the three main financial statements in financial accounting fundamentals, along with the cash flow statement and income statement.

Core Equation

There is only one basic rule that applies to all a balance sheet-and that is the accounting equation:

Assets = Liabilities + Equity

This is the equation that all double entry book-keeping is based on. This is a situation that needs to be kept balanced for every single transaction a business records. When a business purchases equipment on credit from a bank for $500, assets increase $500 (Equipment) and liabilities increase $500 ( Loan payable).

Why It Balances

Due to this equation the balance of the balance sheet is always satisfied. Assets is at a company's owned and utilized assets, which contribute to generating value. Such assets must be acquired from a source such as a creditor's line of credit (liability) or from ownership and net earnings (stockholders or bondholders' equity). By definition, the two sides will always be equal. When the balance sheet does not balance, it indicates a problem in the accounting records; that is why it is important that students double check.

The Three Main Components – Explained Simply

Before getting into the preparation steps, it is important to understand the three “building blocks”. Each and every item that is to be mentioned on balance sheet needs to be divided to three areas which are assets, liabilities and equity. What each of these includes and what goes in and out of each one needs to be understand when one learns about the balance sheet.

Assets

The resources of the business which are expected to benefit the business in the future is called as assets. They are placed on balance sheet on the left side of the balance sheet (or top half), and are listed in two sections:

- Current Assets: These are the assets that are likely to be used within a year or coveted to cash. These include cash, Accounts Receivable, Inventory, and Prepaid expenses.

- Non-Current Assets: These are assets which are not liquidated within one year. These can include assets such as property, plant & equipment (PP&E), intangible assets such as patents and long-term investments.

The principle: Assets first listed are the most liquid (cash) and last listed are the least liquid (land/buildings).

Liabilities

They are financial obligations of the company to other parties, it is what the company owes-it's money that has to be paid back or services that are to be rendered. Likewise assets are divided into current and long-term fixtures, so are liabilities:

- Current Liabilities: Liabilities that will be settled or consumed within a year. Examples include Accrued expenses, Short-term loans, Accounts payable and Unearned revenue.

- Non-Current (Long-Term) Liabilities: Liabilities expected to come due after one year. Examples: Bank loans, bonds payable and deferred tax liabilities.

The amount of debt owed is shown on the right-hand side (or middle column) of the balance sheet, as the claims of creditors are over the assets of the company.

Equity

Equity, which is also referred to as shareholders' equity, is the remaining interest in the assets after deducting all liabilities; or owner's equity-that is, the interest that is left for the owner(s) after paying off all creditors. That is to say, what is left after full settlement of all debts owed by the owner(s). Equity typically includes:

- Owner's Investment / Share Capital: Money that owner(s) have invested in the company or provided to the company as share capital.

- Retained Earnings: Profits that are reinvested into the company without paying a dividend.

- Additional Paid-in Capital (for corporations): For corporations, represents funds from sellers in excess of par value of the shares purchased.

Typically, equity of a small business or a student exercise will consist simply of only the owner's initial investment and gross retained earnings (opening balance + net income − dividends).

Step-by-Step: Preparing a Balance Sheet

With all these parts, let's come up with their combinations. Developing a balance sheet one by one will go a long way towards making the process less frightening. Whether you are dealing with a complete set of accounts or you are only preparing a trial balance to balance sheet format, follow these six steps and you will be able to answer the question in a clear and understandable manner.

Step 1 – Gather the Trial Balance or Account Balances

The first step is to gather all of the financial facts you'll need. In every type of accounting exercise, or in a real world scenario, you will have a trial balance, which is a list of the accounts in the ledger and their balances on a given date. A trial balance is prepared to make sure that the total of the debts equals the total of the credits prior to starting to make any financial statements.

When there is no trial balance, gather the numbers for individual accounts straight from the general ledger. Ensure that the data are current - all the data should show the same date and being reflected in the balance sheet ought to be meaningful and complete.

Step 2 – Identify Assets, Liabilities, and Equity

After your list of balances, identify each on the list. Determine whether this is a business asset, a business debt (liability) or a remaining claim of the owner (equity).

The common accounts and classification of accounts:

- Cash → Current Asset

- Accounts Receivable → Current Asset

- Inventory → Current Asset

- Equipment → Non-Current Asset

- Accounts Payable → Current Liability

- Bank Loan (long-term) → Non-Current Liability

- Owner's Capital → Equity

- Retained Earnings → Equity

This is important because otherwise it is going to mess up all your statements. Spend time here.

Step 3 – Organize into Current vs. Non‑Current

Once you have classified accounts, place them in order of the other accounts within their classified group. This one is the key that makes difference between a simple balance sheet and a good classified balance sheet, which is required for school and work-related situations.

- Under Assets: In the Assets section list the current assets first and then the non-current assets.

- Under Liabilities: List current liabilities first, then long-term liabilities

- Under Equity: List capital contributions, then retained earnings

This ordering has been in line with the standard accounting practice and simplifies the analysis and comprehension of the statement.

Step 4 – Calculate Totals

Sum the values that are contained in each sub-section:

- Total Current Assets

- Total Non-Current Assets

- Total Assets (Current + Non-Current)

Then repeat the steps with the equation for liabilities and equity:

- Total Current Liabilities

- Total Non-Current Liabilities

- Total Equity

- Total Liabilities + Equity

Double-check every addition. The most common problem that causes a balance sheet to not balance is a simple mistake in arithmetic.

Step 5 – Verify the Equation

Now, use on the golden rule for financial accounting basics:

Total Assets = Total Liabilities + Total Equity

When there is an equal number on both sides, your balance sheet will balance. If not, back up and check for the following:

- Missing accounts

- Records in the wrong category

- Arithmetic errors in totals

- Net income excluding transfers to retained earnings.

Wait until sides are even before proceeding on to formatting.

Step 6 – Format the Statement

The proper format of a balance sheet is:

- Heading: A statement title ("Balance Sheet"), the company name, and date ("As of Date") put on the heading.

- Asset Section: Clearly labeled with subtotals

- Liabilities Section: Clearly labeled with subtotals

- Equity Section: Clearly labeled with totals

- Final Verification Line: Total Assets = Total Liabilities + Equity

Use clearly labelled, consistent indentation, currency symbols. Neatness and structure is important – particularly in academic submissions.

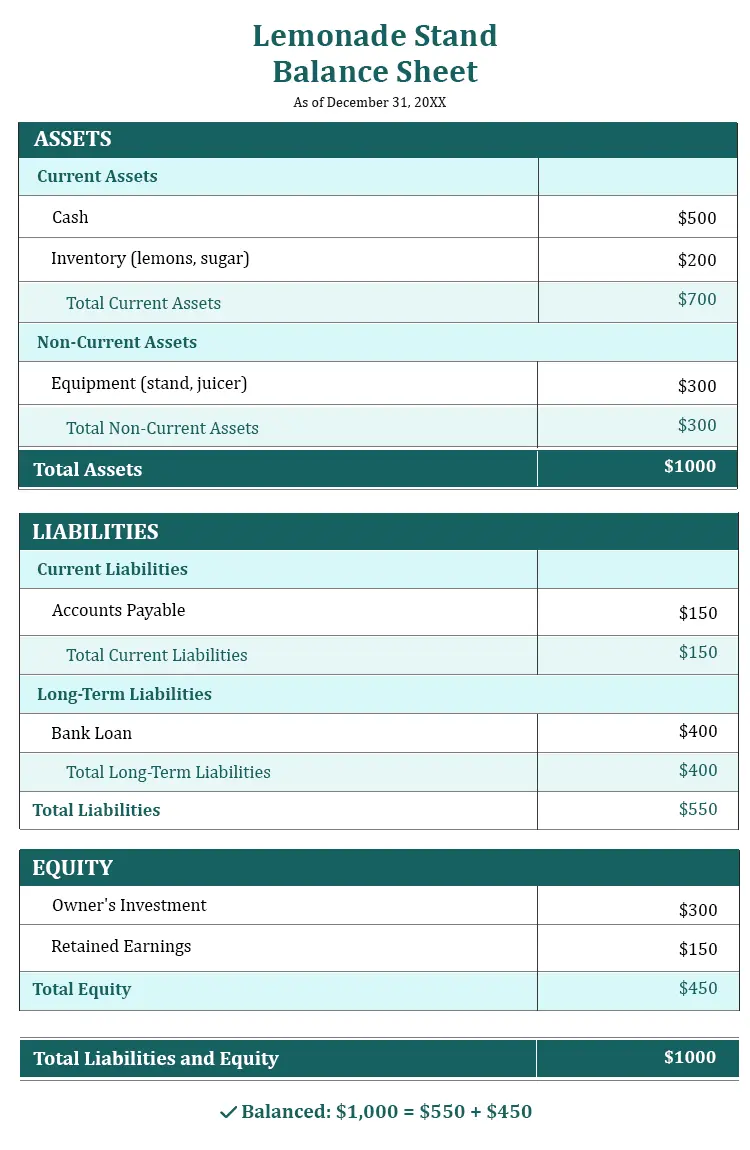

Example – Building a Balance Sheet from Scratch

The easiest way to master the process is to go through an actual example. The following balance sheet example talks about a simple business selling lemonade-a business concept that is easy to follow and has just enough features to show all the major elements of a balance sheet. If your coursework deals with bigger organizations, the same principles would still be in place.

Given Information (Lemonade Stand)

The balance of accounts of the lemonade stand business at the end of the period were as follows:

- Cash: $500

- Inventory (lemons, sugar): $200

- Equipment (stand, juicer): $300

- Accounts Payable: $150

- Loan from bank: $400

- Owner's investment: $300

- Retained Earnings (starting): $100

- Net income for the period: $50 (already added to retained earnings so Retained Earnings = $150)

Step‑by‑Step Solution

The six steps mentioned above must be used on this data:

- List Assets: Cash $500 + Inventory $200 + Equipment $300 → Total Assets = $1,000

- List Liabilities: Accounts Payable $150 + Bank Loan $400 → Total Liabilities = $550

- List Equity: Owner's Investment $300 + Retained Earnings $150 → Total Equity = $450

- Verify: $1,000 = $550 + $450

The equation holds. There's a perfect balance on the balance sheet.

Final Balance Sheet

This is organized and neat – more of what your professor or examiner is looking for! See that each section is clearly labelled and indented and will have a total at the end.

Common Mistakes Students Make

Despite having good amount of knowledge large number of students face issue in making their balance sheet equal. When learning balance sheet for beginners it is very crucial that you keep in mind the common errors to avoid making mistakes. Here is the list of most common errors and what to do about them!

10 Common Balance Sheet Mistakes and How to Avoid Them | Mistake | Why It Happens | How to Avoid It |

| Balance sheet doesn't balance | The number given is incorrect or an account does not exist. | Recalculate all totals; make sure that net income is deposited in retained earnings. |

| Mixing up current and non-current. | Misinterpreting asset life span or due date. | Use rule of one year - current = due/used within 12 months. |

| Forgetting to add net income to retained earnings | Avoiding income statement step | Always finalize the income statement first; carry net income into equity |

| Accounting for revenue or expenses on the balance sheet | Mixing up income statement accounts and balance sheet accounts. | The revenues and expenses are allocated to retained earnings — never shown directly |

| Including dividends as an expense | Viewing dividends as “as if” a cost. | Do not consider dividends an operating expense, they decrease retained earnings. |

| Using an incorrect date | Typing the incorrect period end date | Verify the date of the trial balance and follow this throughout the trial balance |

| Not labeling sections clearly | Rushing formatting | Do use some standard Headings – current assets, non current assets etc. |

| Double-counting an account | Listing an account in both assets and liabilities | Every account is in only one category — classify once |

Some basic accounting principles should be taught and mastered before the formats alone when teaching financial accounting basics. The sense and reason behind the use of the equation is more important than just completing templates.

Balance Sheet Template

Often students learn more when they use templates to practice. A simple template facilitates information to be organized systemically and helps to avoid formatting confusion.

This is a simple template which students can follow for their assignments or practice papers.

Balance Sheet Template

This balance sheet format is very similar to what you'll see in your textbooks, tests and when you become an accountant.

Still Struggling? Get Accounting Homework Help

With practice, compiling a balance sheet is much easier, but sometimes, even after all the guides and tutorials are read and you've followed them, you still feel like you can't do it. This is 100% natural. Learning a skill like Accounting is done over a period of time and it's ok to seek advice or assistance from experts when the concepts aren't getting through.

Whether assignments are overwhelming, deadlines are pressing or there are complicated accounting solutions that include adjusting entries, depreciation schedules and multi-step financial statements, our professional accounting homework help solution can make all the difference.

We have a team of excellent accounting experts and subject specialist who can take you through problem step by step, explaining the reasoning behind each step and line item in your assignment, and keep you on track from start to finish in meeting your deadlines.

From handling a single balance sheet problem to assisting you all the way through an accounting course, we have the homework help you're looking for and we're here with the same aim of assisting you: to understand the material, not just the answer.

Contact us today and we will ease your burdens associated with accounting tasks.